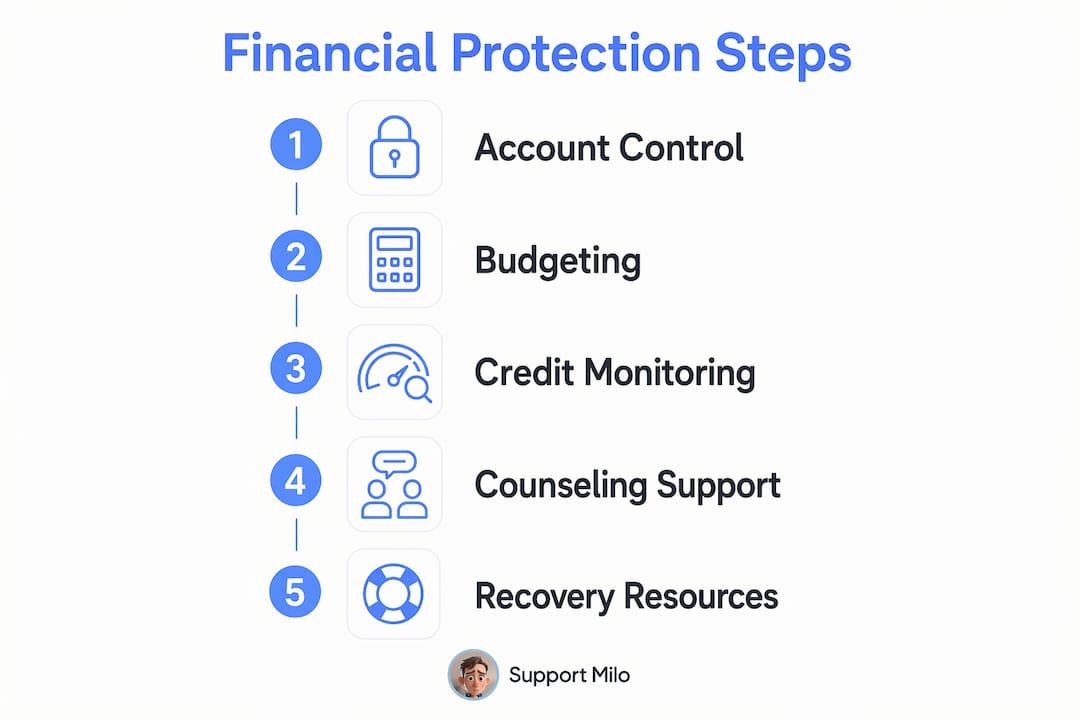

Protecting your family finances from gambling harm means taking direct control of account access, credit exposure, and spending before losses compound. Gambling disorder is defined by the negative impact it creates across life areas, including finances, not by the dollar amount lost or won. That distinction matters because it means financial harm starts early, often before a family recognizes the full picture. The good news is that specific, proven strategies, from locking down shared accounts to accessing free counseling through the Minnesota Alliance on Problem Gambling, can stop the damage and rebuild stability. This guide walks you through every layer of protection, step by step.

What immediate financial controls can families implement to limit gambling access?

The fastest way to protect family finances from gambling is to reduce the gambler's direct access to money and credit. Every day that access remains open is another opportunity for losses to grow. Experts recommend changing banking passwords and PINs immediately as a first line of defense, alongside adjusting account signatories so that one person alone cannot move large sums.

Here are the core financial controls families can put in place right away:

- Transfer account management to a trusted person. Have a non-gambling family member take primary control of debit cards, checkbooks, and online banking credentials.

- Require multiple signatories on shared accounts. This means no single person can authorize large withdrawals or transfers without a second approval.

- Close or reduce credit card limits. Cancel unnecessary credit cards entirely, and call issuers to lower limits on cards that remain open.

- Switch to prepaid cards or daily withdrawal caps. A prepaid card loaded with a set weekly amount creates a hard ceiling on spending without cutting off access to necessities.

- Lock valuables and financial documents. Passbooks, spare cards, and investment statements should be stored securely, away from easy access.

- Set up account alerts. Most banks allow text or email notifications for every transaction above a set threshold. Use them.

These steps are not about punishment. They are about creating a structure that makes impulsive gambling harder while the underlying issue is being addressed. Setting clear financial boundaries also increases the likelihood that the person struggling with gambling will engage with treatment, because the financial pressure is reduced and the family's trust is partially restored.

Pro Tip: Open a separate household expenses account in the name of the non-gambling partner only. Direct all income into this account first, then transfer a fixed personal allowance to the person in recovery. This keeps bills paid while preserving dignity and autonomy.

How can budgeting help protect your family from gambling losses?

A realistic household budget is one of the most powerful tools for gambling financial protection because it makes the true cost of gambling visible. When every dollar is assigned a purpose, there is no ambiguous "extra" money that can quietly disappear into a betting app or casino. Financial counseling for gambling harm focuses specifically on building these budgets alongside debt management plans, which is a different skill set from general financial planning.

Follow these steps to build a budget that actively protects your family:

- List all income sources. Include wages, benefits, freelance income, and any regular transfers. Use net figures, not gross.

- Map every fixed expense. Rent or mortgage, utilities, insurance, and loan repayments come first. These are non-negotiable.

- Identify variable expenses. Groceries, transportation, and childcare costs should be estimated conservatively, using the last three months of bank statements as a guide.

- Calculate the gap. Subtract total expenses from total income. If the number is negative, you have a debt problem that needs a counselor, not just a spreadsheet.

- Set a gambling spending limit of zero. The Wisconsin Department of Health Services advises betting only what is affordable and never borrowing to play. For families in crisis, the affordable amount is zero until stability is restored.

- Separate finances where possible. Keeping individual accounts distinct reduces cross-exposure, meaning one person's relapse cannot drain the entire household.

| Budget Category | Recommended Action |

|---|---|

| Fixed expenses | Pay automatically from a protected account |

| Variable expenses | Use a prepaid card with a weekly cap |

| Debt repayments | Consolidate and manage through a counselor |

| Savings | Automate a small fixed transfer, even $10 per week |

| Gambling spending | Set to zero during active recovery |

Structured financial counseling tailored to gambling-related stress reduces emotional and financial burdens faster than generic budgeting advice. That is because gambling-specific counselors understand the shame, secrecy, and distorted money beliefs that come with the disorder. They address those directly, not just the numbers.

Pro Tip: Use a free app like Mint or YNAB (You Need A Budget) to track spending in real time. Seeing transactions update live makes it much harder to rationalize small "harmless" bets that add up fast.

Why is monitoring credit reports essential during gambling-related financial risk?

Credit monitoring is the early warning system for hidden gambling losses. Many families discover the true scale of gambling debt only when a loan application is denied or a collection notice arrives. By that point, months of damage have already accumulated. Checking credit reports regularly via AnnualCreditReport.com gives you free access to reports from Equifax, Experian, and TransUnion once per year, and more frequently if you suspect fraud.

Watch for these specific warning signs on credit reports:

- Unrecognized accounts or credit inquiries. A new credit card or personal loan you did not authorize is a serious red flag.

- Sudden drops in credit score. A score drop of 30 or more points in a single month often signals missed payments or new debt.

- Maxed-out credit lines. Utilization above 90% on any card suggests someone has been drawing on credit to fund gambling.

- Accounts in collections. These appear when debts have gone unpaid for 90 to 180 days, meaning the problem started much earlier.

| Credit Signal | What It May Indicate |

|---|---|

| New unrecognized account | Unauthorized credit application to fund gambling |

| High utilization rate | Repeated cash advances or maxed cards |

| Missed payment history | Income diverted to gambling instead of bills |

| Collection notices | Long-term hidden debt now surfacing |

If you find errors or fraudulent accounts, the FTC's guidance on disputing credit report errors explains exactly how to file disputes with each bureau. The process is free and legally protected. Acting quickly limits the long-term damage to your family's credit health and borrowing capacity.

What support resources can help families rebuild finances after gambling harm?

Recovery from gambling-related financial harm does not have to happen alone. Several national and community resources exist specifically to help families stabilize their finances and access treatment. Knowing where to turn is half the battle.

The most direct starting point is the National Problem Gambling Helpline, which launched its new number, 1-800-MY-RESET, nationwide in 2026. The line is free, available 24 hours a day, and connects callers to trained local resources. It is designed as a stigma-free access point, meaning anyone worried about a family member's gambling can call, not just the person with the disorder.

For financial-specific support, the Minnesota Alliance on Problem Gambling offers up to six free confidential sessions with counselors who specialize in gambling-related financial harm. These sessions are available to both gamblers and their family members. The counselors help with debt management, credit rebuilding, and reducing the money-related tension that often fractures families during recovery.

Clinical treatment resources add another layer. The National Council on Problem Gambling's Stage III training program emphasizes that family and money mindset work are clinical care components, not optional add-ons. This means the best treatment programs actively involve family members in conversations about financial behavior and beliefs, not just the gambling behavior itself.

"Gambling harm is not defined by amounts lost or won, but by negative impacts on life areas including finances. Early financial protection measures matter even when losses seem small."

Community and nonprofit programs round out the support picture. Organizations like From Love With Care provide welfare and support services that can assist vulnerable family members navigating the isolation that often accompanies gambling crises. Support-milo itself offers a community-driven platform where families can track debt repayment progress, share stories, and access encouragement through the Hope Wall. These community touchpoints matter because recovery is rarely a straight line, and having people around you who understand the journey makes a real difference.

Key takeaways

Protecting family finances from gambling requires immediate account controls, structured budgeting, active credit monitoring, and access to specialized counseling resources working together.

| Point | Details |

|---|---|

| Lock down account access first | Transfer card control to a trusted family member and require dual signatories on shared accounts. |

| Build a gambling-specific budget | Assign every dollar a purpose and set gambling spending to zero during active recovery. |

| Monitor credit reports proactively | Check Equifax, Experian, and TransUnion reports for unrecognized accounts or sudden score drops. |

| Use free specialized counseling | Minnesota Alliance on Problem Gambling offers up to six free sessions for gamblers and family members. |

| Call 1-800-MY-RESET for immediate help | The National Problem Gambling Helpline connects families to trained local resources 24/7 at no cost. |

What I've learned about financial protection and gambling recovery

Working alongside families navigating gambling harm, I've noticed one pattern more than any other: the financial safeguards that work are the ones put in place before the next crisis, not after. Families often wait until a major loss or a discovered debt to act. By then, the emotional damage makes clear-headed financial decisions much harder.

The most effective approach I've seen combines two things that most people treat as separate: clinical treatment and financial restructuring. Involving family in money mindset discussions is now recognized as a clinical priority, not just a practical one. When a family sets up a protected account structure and simultaneously engages with a counselor, the recovery sticks more often and more quickly.

I also want to say this directly: setting financial boundaries is an act of love, not control. When you remove easy access to shared funds, you are not punishing the person struggling. You are removing a trigger and protecting the people who depend on you. That reframe matters enormously for family cooperation. Families who approach these conversations with empathy, rather than blame, get better results every time.

One more thing. Credit monitoring is consistently underused by families in this situation. People assume they would know if something was wrong. They often don't. Hidden gambling debts and unauthorized credit accounts surface months after the fact. Make it a monthly habit, not a one-time check. Your future self will thank you.

— Milo

How Support-milo can help your family take the next step

If your family is dealing with gambling-related financial stress, you do not have to figure it out alone. Support-milo is a nonprofit community platform built specifically for people navigating gambling harm and debt recovery together.

Through Support-milo's enterprise resources, families can access confidential counseling, budgeting guidance, and debt management support tailored to gambling-related challenges. The platform's Hope Wall offers real encouragement from people who have been exactly where you are now. You can track debt repayment progress, share your story, and connect with a community that genuinely understands. Whether you are just starting to recognize the problem or already deep in recovery, Support-milo is here to walk alongside you.

FAQ

What are the first steps to protect family finances from gambling?

The first steps are to transfer account control to a trusted non-gambling family member, change online banking passwords, and reduce or close unnecessary credit lines. These actions limit further financial exposure while longer-term recovery plans are put in place.

How do I get a free credit report to check for gambling-related debt?

You can access free annual credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com. The FTC advises reviewing all three reports for unrecognized accounts, missed payments, or sudden score drops that may signal hidden gambling debt.

Is there free financial counseling for families affected by gambling?

Yes. The Minnesota Alliance on Problem Gambling offers up to six free confidential financial counseling sessions for both gamblers and their family members, focusing on debt management, credit rebuilding, and reducing family financial tension.

What is the National Problem Gambling Helpline number in 2026?

The National Council on Problem Gambling launched 1-800-MY-RESET as the new National Problem Gambling Helpline number in 2026. It is free, available 24/7, and connects callers to trained local support resources without judgment.

How does budgeting help prevent gambling losses from harming the family?

A structured budget assigns every dollar a specific purpose, eliminating the ambiguous "extra" money that often funds impulsive gambling. Setting a gambling spending limit of zero during recovery, combined with automatic bill payments from a protected account, creates a financial structure that reduces relapse risk.